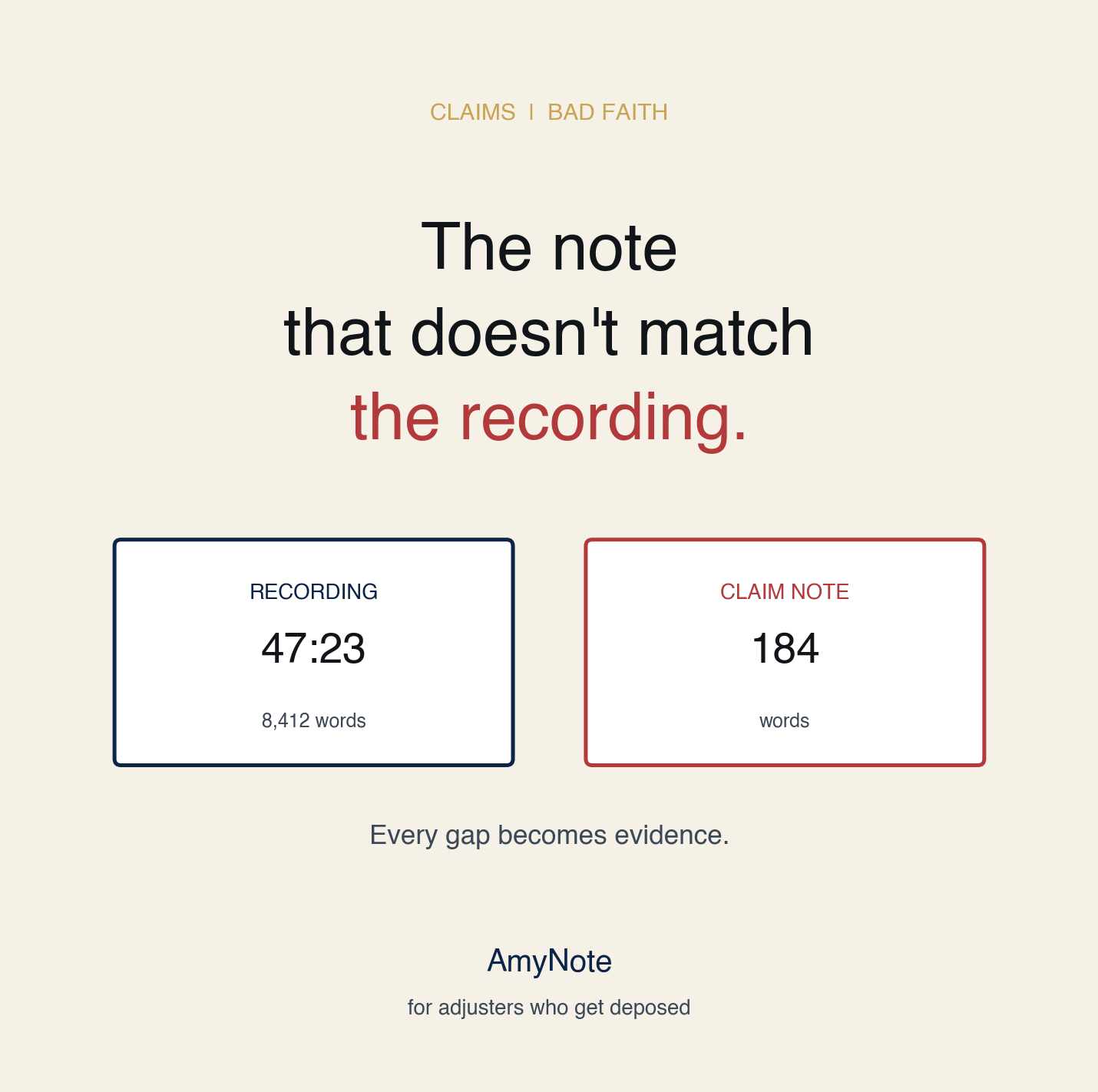

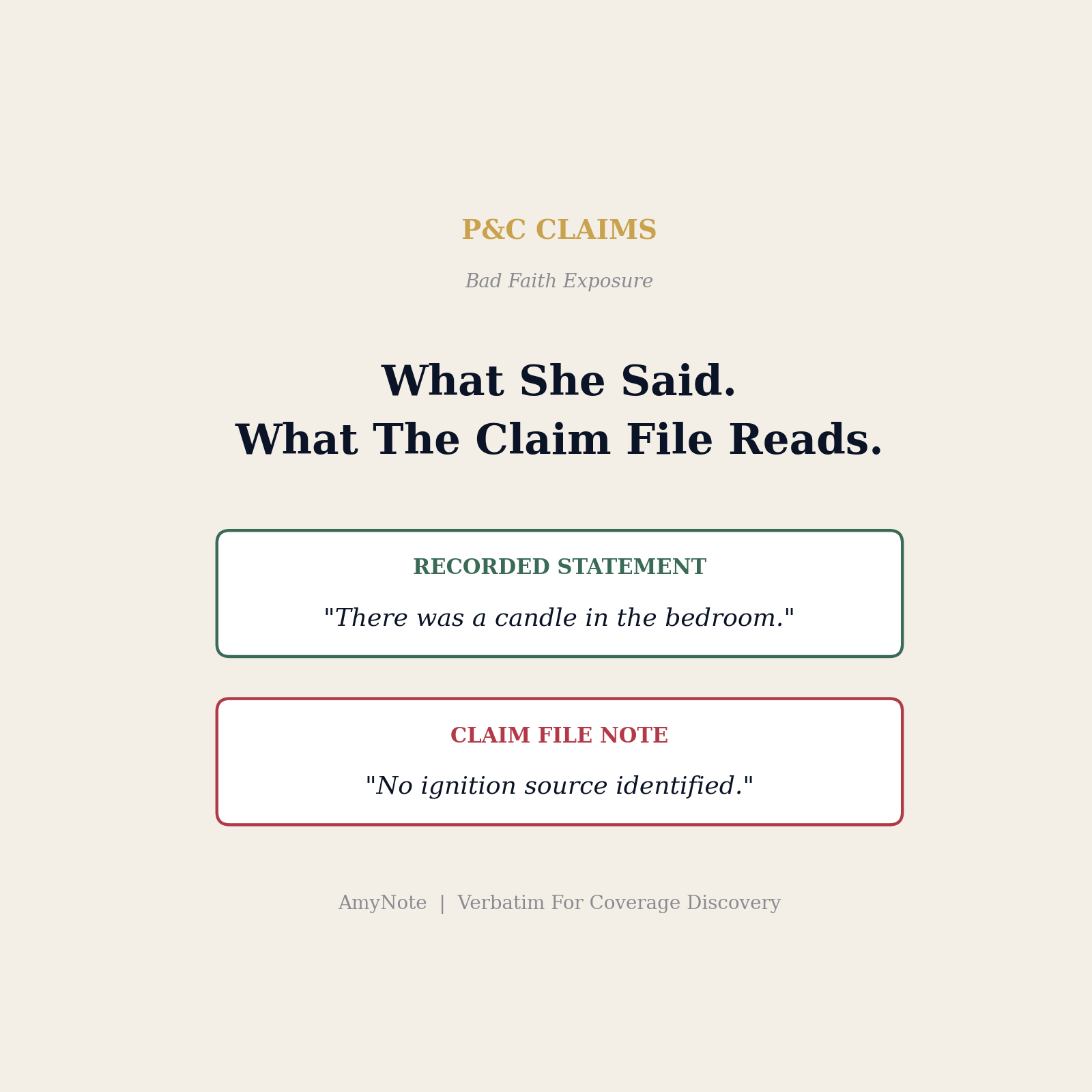

A homeowner gives a 47-minute recorded statement to your fire adjuster on day three after the loss. She mentions a lit candle in the bedroom at minute 31. Two years later in coverage litigation, plaintiff's counsel pulls the audio. The contemporaneous claim file notes, typed by the same adjuster, read "no ignition source identified, cause undetermined." The jury sees the gap. Bad faith. Four million in punitive damages on top of a $480,000 dwelling claim.

This is not an outlier story. It is the structural shape of how first-party property losses are documented in 2026. The recorded statement is the contractually compelled evidence. The typed summary is the working record. The audio is the buried record. Counsel finds the gap years later. The gap is the case.

The Problem: Two Records, One Set Of Words

Property and casualty adjusters take recorded statements under the Unfair Claims Settlement Practices Act framework adopted in 49 states (NAIC Model Act 900). The statement is a contract right under the policy cooperation clause. State law gives the carrier 15 to 30 days to acknowledge the claim, 30 to 60 days to investigate, and a continuing duty of good faith and fair dealing that survives every claim decision and outlives the file.

The adjuster records the call on a third-party platform like Davies Group, LexisNexis ClaimSearch, or whatever the carrier's recorded-statement vendor of the month happens to be. She then types a summary into the claims system — Guidewire ClaimCenter, Duck Creek Claims, Snapsheet, Hyland OnBase — so the next handler, the supervisor, the SIU referee, and the coverage attorney can pick up the file without re-listening to 47 minutes of audio.

The audio gets archived to a vendor bucket nobody opens again. Until litigation discovery two or three years later, when plaintiff's bad-faith counsel sends a single-line request: "Produce all recorded statements taken in connection with claim number XYZ."

The summary is the working record. The audio is the buried record. The gap is the bad-faith case.

What The Gap Actually Looks Like

The gap rarely shows up as an outright contradiction. It shows up as omission, paraphrase drift, and the natural compression that happens when 47 minutes of recorded conversation gets typed into a three-paragraph free-text field on the same day the adjuster has eleven other inspections to close.

- Omission. The insured mentions, in passing, that the candle was "one of those big jar ones I got from Yankee" before pivoting to the smell of smoke when she came home. The adjuster types "homeowner returned to property and observed smoke." The candle never makes the summary because the homeowner moved on quickly and the adjuster was tracking the timeline, not the ignition source.

- Paraphrase drift. The insured says "I had a candle going in the bedroom but I think I blew it out." The adjuster types "homeowner unsure whether candle was extinguished prior to leaving." Two years later the plaintiff lawyer plays the audio side-by-side with the file note, and "I think I blew it out" reads as a deliberate softening to support a coverage decision.

- The forced conclusion. The cause-and-origin paragraph at the bottom of the summary template demands a determination. The adjuster, syncing fact and template, types "cause undetermined" even though the recorded statement contains three separate references to candles, space heaters, and a frayed extension cord. The template wrote the conclusion. The audio remembers everything.

None of this is bad-faith conduct in the moment. It is the predictable, repeated output of a claims operation that asks its adjusters to be both interviewer and stenographer in the same shift, then files the audio to a vendor archive nobody opens again.

Why Current Solutions Fail

Carrier transcription contracts price out at $1.50 to $3.50 per audio minute. A single complex homeowner loss generates two to four hours of recorded statements across the insured, witnesses, the public adjuster, and the neighbors. Multiply by a 600-claim desk and per-statement transcription becomes a six-figure annual line item that nobody approved — so the contract gets used only on flagged SIU files and the rest of the desk stays summary-only.

Speech-to-text plugins built into Guidewire and Duck Creek exist and have improved meaningfully over the last two years. They ship raw, unstructured transcripts with no speaker labels. The adjuster still types a summary because the raw transcript is not searchable or citable in a coverage opinion letter, and the supervisor will not read 47 pages of single-spaced dialogue to approve a denial. The transcript becomes shelf-ware. The summary remains the working record.

Outsourced human transcription returns in five to ten business days. The investigation clock under UCSPA runs in real time, and most internal claim guidelines compress the typed summary to 24 hours after the statement is taken. The summary gets typed from memory. The audio is filed. Then it sits.

The structural failure is not that transcription is hard. It is that the typed summary and the recorded audio live on different timelines, written by different processes, with no contractually enforced relationship between them. The summary is what the human remembered. The audio is what the human actually heard. Counsel for the insured needs only to play both.

What The Carrier Side Of A Bad-Faith Case Looks Like

Bad-faith doctrine across U.S. jurisdictions broadly asks three questions: did the carrier conduct a reasonable investigation, did the carrier have a reasonable basis to deny or delay the claim, and did the carrier act with knowledge that its position lacked a reasonable basis. The insured does not need to prove the carrier was malicious. The insured needs to show the investigation cut corners or that the file does not match the words.

The recorded statement is the single most powerful piece of evidence in establishing both. It is verbatim. It is contemporaneous. It is contractually compelled under the cooperation clause, which means the insured cannot later argue the words were taken out of context. And it is sitting in a vendor archive that the carrier's own retention policy guarantees will still be there when discovery requests arrive in year three.

When the file summary and the audio diverge, the insured's lawyer does not need to allege motive. The divergence does the work. The summary is the carrier's narrative. The audio is the underwriter of that narrative. A jury that reads both and sees the gap will fill in the motive on its own.

What Actually Works

The adjuster records the statement in the field or over the phone, and an on-device speech model transcribes verbatim in real time. Every "I think," every "maybe," every reference to a candle, a space heater, a prior loss, gets timestamped and speaker-labeled. The transcript is searchable by claim number, peril keyword, and policy exclusion language at the moment the file is opened.

When the adjuster drafts the statement summary that lands in ClaimCenter, every factual assertion cites a transcript line. The summary and the audio say the same thing because the summary was generated from the transcript, not from memory three hours later. The supervisor reviewing the file can spot-check any sentence by clicking the citation and reading the line in context. The cause-and-origin paragraph either cites the transcript or it does not get written.

AmyNote runs the audio pipeline through OpenAI's latest Speech API with diarization, and the summary model through Anthropic's Claude Opus. Both OpenAI and Anthropic contractually guarantee zero training on user data. Audio is encrypted in transit, not retained on provider servers after processing. Transcripts and recordings are stored locally on the device with end-to-end encryption. The cooperation-clause statement never leaves the adjuster's phone.

When plaintiff's counsel pulls the audio in year three, the claim file already cites the candle. The investigation reads as good faith on the record. The cause-and-origin paragraph is the same paragraph the insured listened to during the statement. The bad-faith claim collapses before it gets to the jury, because there is no gap left to walk through.

The Documentation Pattern That Holds Up

A defensible recorded-statement workflow has four properties. None of them are about the technology and all of them are about discipline.

- One audio, one transcript, one summary, all linked. The summary cites transcript lines. The transcript references the audio file. The audio file lives in the claim record, not on a vendor shelf nobody can find.

- The summary is generated, not remembered. The summary is drafted from the transcript by an AI model that can be re-run, audited, and reviewed. It is not typed from a notepad three hours after the call.

- The cause-and-origin paragraph is grounded. Every factual assertion in the determination paragraph either cites a transcript line or marks the omission as "not addressed by insured." The template never forces an unsupported conclusion.

- The privacy posture matches the privilege. The recorded statement is sensitive policyholder data. The transcription pipeline must be contractually zero-training, the audio must not be retained by third parties, and the transcripts must be encrypted at rest.

Carriers that adopt this pattern do not eliminate bad-faith litigation. They eliminate the specific kind of bad-faith litigation that turns on the gap between the file and the recording. That is the most expensive category, and it is the category that produces the punitive verdicts.

Getting Started

Open AmyNote at the start of every recorded statement. Confirm consent on the audio so the cooperation-clause use is contractually clean. Let the transcript run. Draft the ClaimCenter summary directly from the verbatim transcript, citing line numbers in the file note. Hand the next adjuster, the coverage attorney, and the plaintiff's lawyer the same words your insured actually said.

When the deposition comes in year three, the file does not contradict the audio. It is the audio.

Originally published as an X Article.